Tax-Free Retirement

|

Wars, social programs, wasteful government spending, heavens to Betsy! Where are they going to get the money to fund all this? If you think Washington is at a loss as to how and where to find these funds… think again!

When we take a 30,000-foot view of the plans the government offers for your retirement years, it becomes abundantly clear that you’re creating a joint account with the IRS to help them fulfill their funding needs! What do we mean by this? Well, to break it down let’s look at the 4 traps that come along with these “helpful” government sanctioned plans. 1. The Tax Trap

You may be single or married with kids. You may make $30,000 a year or $300,000 per year. You may be a corporate executive, have a blue-collar job, or run a business out of your home. It’s really doesn't matter. What matters is that you understand all the issues at play, because they effect you in the same way.

We’re going to explore the dangers that make up The Tax Trap; dangers that could potentially destroy the financial golden years of your life. At retirement most of the accumulated savings in a qualified plan will be gain… by a wide margin! And that’s not the problem. The problem lies in how much of that gain will actually be yours. Let’s take a look…

You see what just happened there? In this example (that sadly, is all too typical) the $7,200 tax deferral - costs them nearly seven times more in actual taxes to be paid than what they saved in taxes! That doesn’t seem like a benefit to us! See why we classify this as a trap? At the time of this writing the government is 21 trillion dollars in the hole and currently there is 24 trillion dollars sitting in qualified plans; you do the math. Realize that at anytime they can raise the tax rate on distributions and get what they need from these ‘low hanging fruit’ plans. It’s just too easy! But we digress, let’s move on to the second trap. Watch Video 2. The Access Trap

Who would agree that all phases of our lives need funding; not just the retirement phase? From purchasing our first car, to buying a home, to starting a family, to paying for college and lastly, retirement. With everything we know we’ll be facing, financially, through the years, does it really make sense to lock our money away where we can’t access it without heavy penalties and fees? Life takes cash and lots of it!

For the Access Trap we’re going to look at trying to pay for college with qualified plan funds. Spoiler alert… yikes! In this hypothetical scenario let’s take a look at a 50-year-old father that wants to help fund his daughter’s college education. Because this father is still working and earning a good income, $130,000 a year, every dollar he pulls out of his retirement plan is added to his existing income, taking him into a higher marginal tax bracket very quickly. So let’s say that higher tax bracket he’s in now is 33% because it took his taxable income to over $200,000 (as of 2018). He also has a 10% state tax and a 10% early withdrawal tax penalty. Therefore, this father must fork over 53 cents of every dollar to the IRS to pull money out of his retirement account before age 59½. Fifty-three cents! So this is what it looks like for him:

Do you think this dad is frustrated? Do you think he feels his money is being held hostage? Would you? To have to pay more in taxes and penalties to access the funds than the cost of the tuition itself is maddening! When you step back and see this reality in black and white it really does look a bit criminal, doesn’t it? The bottom line for The Access Trap is the costs can be steep for not having control and liquidity of your money. So when using these plans you're helping to create a financial prison for your money and the conditions of it’s release are penalties, fees and taxes. Oh, my! 3. The Distribution Trap

There are many laws that govern how this part plays out for individuals, but all you need to know is how ‘The Distribution Trap’ works and how it can affect your future. In plain terms, the IRS wants to get its hands on its retirement. Yes, the account does have your name on it, but when 30%, 40% or even 50% of your distribution can wind up in Uncle Sam’s hands, you gotta step back and wonder, “Whose retirement is this anyway?” Remember that joint account I mentioned.

Here’s how it works. By April 1st after the year you reach 70½ you MUST begin taking a required minimum distribution (RMD) from your tax qualified retirement account, whatever type you have. But, don’t worry the government and the company that manages your plan will have all the numbers figured out for you. So what happens if you don’t take the mandatory distribution? Well, lets read the answer straight from IRS Publication 590-B. It reads:

To Recap...

Q. Where is most retirement money today?

A. In qualified retirement plans. To the tune of trillions of dollars. Q. Can I get my money out of my account before age 59½ A. Not without penalties. And under some special circumstances, you can, if you systematically liquidate your account over several years, but for all intents and purposes, you cannot. Q. If I do take money out before age 59½ what happens? A. On top of the substantial tax you would have to pay, you also incur a 10% penalty. Q. After I reach age 59½ can I get my money out tax-free? A. Sorry, no again. Every penny in a tax-qualified account (including your original contributions) will be taxed at your current tax bracket at the time of withdrawal. Q. What if I don’t need the money in retirement? Can I let it accrue in my account and pass it along to my heirs? A. Once again, no. Regardless of whether you need the money or not, you MUST begin withdrawing it in the year after you reach age 70½. Q. What about at death? How does this account get taxed? A. Glad you asked. That’s Retirement Trap #4 – The Death Trap. If you thought the other traps were bad, wait until you hear this one. 4. The Death Trap

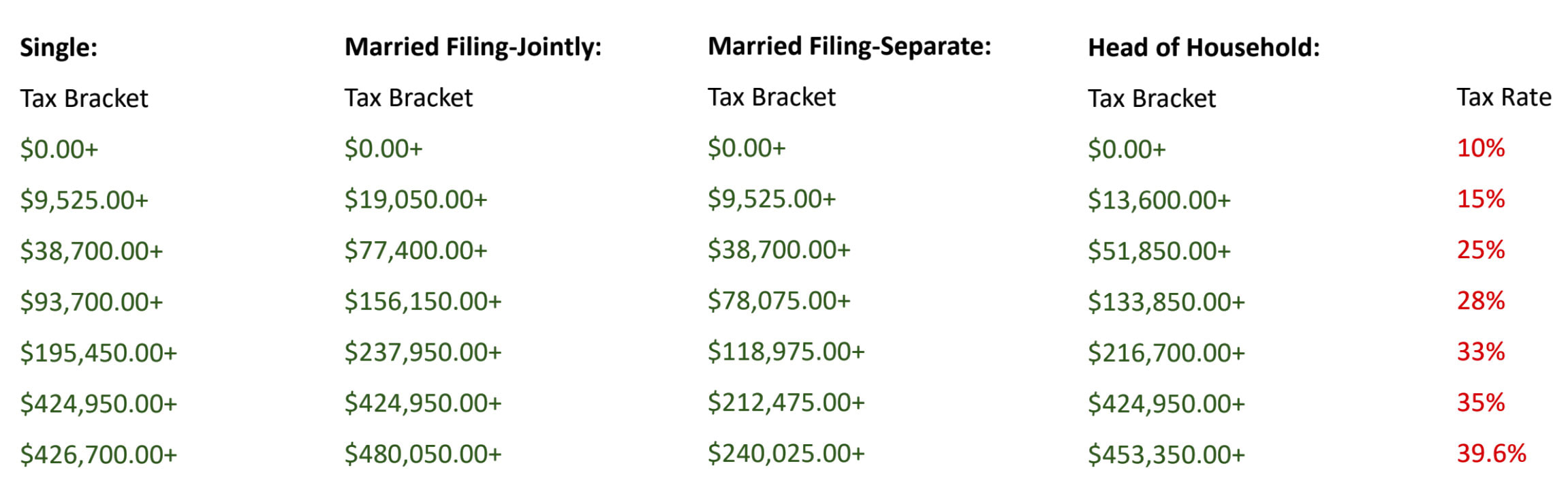

“Iceberg right ahead!” was the infamous statement of the British sailor and survivor of the RMS Titanic on April 14, 1912. Have you ever thought what would happen if you hit an iceberg? Not literally like the Titanic, but figuratively. We all have Icebergs lurking in our financial waters. Each one eager to sink and destroy. Those participating in tax-qualified plans have to stop and think about what happens when they hit the granddaddy of all icebergs – the Death Iceberg? No matter when they hit it, tomorrow, in ten years or at a ripe old age, one thing’s for sure this is an iceberg they all will hit. And when they do what will be left behind for those they love and who love them? Exactly how does death affect the results of tax-qualified retirement plans? Let’s look at it through the tale of The Two Icebergs of Death; premature death & expected death Iceberg #1 - Premature Death When people are setting up these plans with their financial planner or company’s plan administrator, they’re picturing themselves at some golden age in the distant future. Living out all the dreams they set the retirement account up for. What they’re not picturing is dying tomorrow. No, their picture of the future extends way beyond tomorrow. But, most people don’t stop long enough to ask the crucial question “What if my future is only tomorrow?” A question no one likes to face, so they ignore it, avoid it, pretend the possibility doesn't exist (at least not for them). The lack of planning for premature death has led people to make an all too common, but critical financial error. They don’t leave enough money for those left behind. This shortfall can happen in two ways. Firstly, savings in an account like this has not had the luxury of time and the power of compound interest to work, therefore it’s a fraction of what it’s projected to be 30 years in the future. For example, let’s say a person were able to put away $1,000 per month into one of these tax-qualified plans, they could reasonably expect to build a nest egg of $3M + in 30 years! And that’s the number that sticks in the brain of people starting these plans. But what if all that was cut short? What if they hit the granddaddy iceberg of premature death? What if they’ve only made one deposit of $1,000? That means their account stands at the value of their deposits, so far… $1,000. Even if it didn’t happen for 5 years, their account is still far less than even $100,000 – do you think that’s enough to take care of the surviving family or spouse? This is partially why it’s so crucial to investigate financial plans that are self-completing, meaning part of the contributions are used to purchase permanent life insurance equal to the human life value of the bread winner (anywhere from 10-15 times their annual income, sometimes more). So if the unexpected were to happen early or mid-way through the process your family doesn’t have to suffer financial devastation, too. Not to mention the tax implications that come along with the distributions of tax-qualified plans, while life insurance proceeds are distributed tax-free. Now are we suggesting life insurance as an investment? No. But as a core feature and safety net to any financial plan you put in place. Now let’s look at the other iceberg – expected death. Iceberg #2 – Expected Death For the sake of this illustration we are granting you a long, full life and all your planning & saving has been a worthy undertaking that will now fuel those ‘golden years’ you’ve pondered for so long. Since you’ve saved so diligently in your tax qualified retirement plan – you’ve created a very strong habit of saving. And one thing that has been found to be universally true of good savers is they remain good savers in retirement, too. This may sound hard to believe, but it’s difficult to begin spending the money you’ve spent so long accumulating. Many people don’t make this switch easily. They’re dealing with the fact that their savings must last for the rest of their lives. And who knows how long that’s going to be? With modern medical technologies and healthier lifestyles being propagated just about everywhere, these savers figure out very quickly that even when they do start spending their retirement money, they better conserve it so that it lasts longer than they do! To achieve the level of comfort & security they desire some stretch it out by only spending the growth, or interest, in their account, leaving their original nest egg intact. But in a majority of cases, there is almost always money left in the account at the retiree’s death. Often lots of money! Read this next statement very carefully; it is one of the most profound statements we’re going to make in this article. The single worst place to have money stored at death is in a tax-qualified account. Why? What happens to money in a tax-qualified plan at the time of death? Well, it’s not pretty. As a matter of fact it’s flat-out ugly. There are different tax treatments for different situations; i.e., if the retiree is married, if they’re not married, etc.. If they’re not married or upon the death of the second spouse, the account will get completely obliterated by taxes. So there is no escape. Let’s walk through this coming disaster. The Federal tax rates are broken into different percentages based on varying income bands. In 2018 the Federal income tax brackets look like this:

When you’re talking about a person’s life savings, it doesn’t take much to accumulate an account

worth more than $500,000. And at death (except if passing to a spouse) the entire account gets treated as taxable income paid in that year and gets taxed at the appropriate tax rate. Looking at the Federal tax rate grid, can you tell how a tax-qualified account with $500,000 in it will be impacted? Let me help make the numbers clear for you. At today’s top tax rate a $500,000 account would get hit with $198,000 in federal income tax and another $44,850 in state income tax (if you live in a state with a 9% income tax rate, like Maryland). That’s a staggering $242,850 vaporized in an instant! Hopefully, Uncle Sam’s your favorite uncle, because he just became a nearly 50% heir of your retirement account! Could be more, could be less. But what if you were able to cut him out all together? How would that feel? Because, think about it, who wants to save all their working-adult life with the real possibility of the majority stakeholder at retirement being the IRS? Who would you rather give it to? Your kids? A charity? An alma mater? A favorite niece or nephew? The local dog catcher? Most people would rather give it to ANYBODY before they give it to the government! Bottomline, if you have money in a tax-qualified plan at death, you’re stuck. Uncle Sam will get his cut – he’s chomping at the bit for that day. So what’s the resolve to all this tax-qualified plan doom & gloom? Good news, there is one! We can show you how you can give your money to any person or organization and bypass your greedy uncle. Read this list of features for an account some people use for their retirement savings and as you

go, I want you to mentally check off the ones you’d like your account to have:

I don’t know about you, but we checked every box and if you’re interested in learning more about how one of these accounts can work for you, contact us today! DISCLAIMER: The information, general principles and conclusions presented in this article are subject to local, state and federal laws and regulations, court cases and any revisions of same. While every care has been taken in the preparation of this article, CORE Financial Partners is not engaged in providing legal, accounting, investing or tax advice or services. This article should not be used as a substitute for the professional advice of a qualified professional in any of the aforementioned fields. |